How AI Is Reshaping Personal Finance in 2026: What Actually Works, What Doesn’t, and What to Watch

Artificial intelligence has moved from the edges of personal finance to its centre faster than most people expected. According to Plaid’s March 2026 research, roughly 57% of consumers now expect their fintech apps to use AI, and 78% say they are open to receiving AI-based personal financial guidance. The technology is embedded in the apps millions of people use daily — budgeting tools, investment platforms, fraud detection systems, credit assessments, and insurance pricing — often invisibly, often consequentially.

But the honest picture of AI in personal finance in 2026 is more nuanced than either the enthusiastic marketing or the dismissive scepticism suggests. AI is genuinely transforming some financial tasks in ways that produce measurable value. It is being overstated in others. And it introduces specific new risks — particularly around data privacy and AI-enabled fraud — that most users are not adequately informed about. This article covers all three dimensions: where AI in personal finance delivers real value, where the hype exceeds the reality, and what risks it creates that require active management.

The India-specific context is addressed throughout, because the AI-in-finance story looks meaningfully different in a market defined by UPI, digital banking penetration, SEBI-regulated investment platforms, and a regulatory environment still developing its AI-specific framework.

What AI Is Actually Doing in Personal Finance Right Now

Budgeting and Spending Analysis: The Clearest Immediate Value

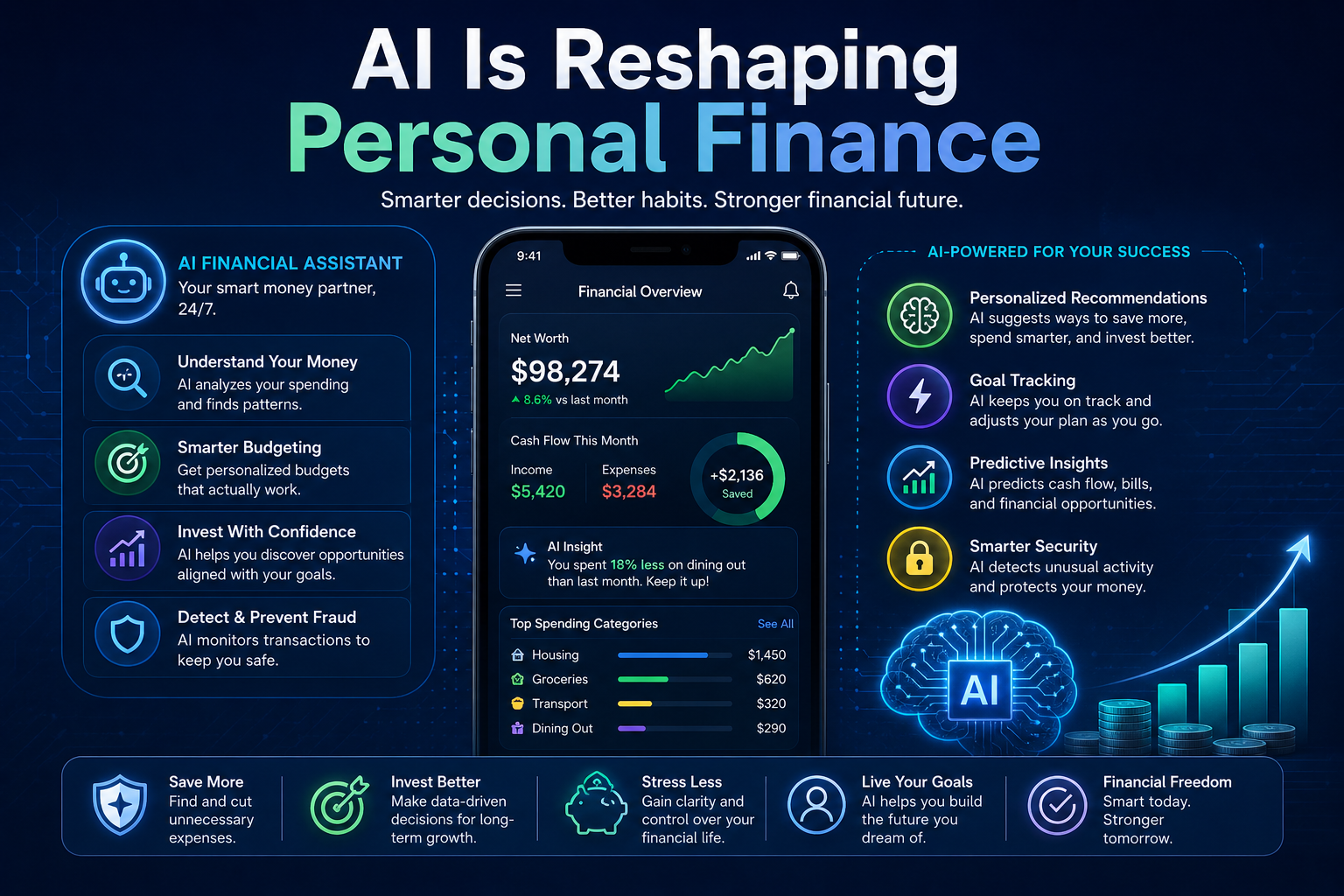

The most immediately useful AI application in personal finance is automated spending analysis — systems that categorise every transaction, identify patterns in expenditure, surface anomalies, and generate insights without requiring the user to manually review bank statements or maintain a spreadsheet.

This sounds modest, but the behavioural impact is significant. The primary reason most people fail to budget effectively is not that they do not want to — it is that manual tracking creates enough friction that consistency is impossible for most people across time. AI-powered categorisation removes that friction almost entirely. When an app tells you at the end of the month that you spent 40% more on food delivery than the previous month, or flags that you have three streaming subscriptions you have not used in 60 days, it is surfacing information that was always technically available in your bank statements but practically invisible because extracting it required work that most people will not consistently do.

In India, the integration of AI spending analysis with UPI transaction data is particularly powerful. UPI’s real-time transaction infrastructure means that AI tools connected to UPI-linked accounts have access to an unusually complete picture of spending — covering a broader range of transactions than debit or credit card data alone. Applications like Fi Money, Jupiter, and INDmoney use AI to categorise UPI transactions, identify spending trends, and surface recommendations based on transaction history. These are not generic recommendations — they are generated from the user’s actual financial behaviour, which is the meaningful differentiator from generic personal finance advice.

The limitation of current AI budgeting tools is the quality of their recommendations beyond categorisation. Surfacing a spending pattern is useful; the suggested response to that pattern is only useful if it accounts for the full context of the user’s financial life — income variability, existing commitments, financial goals, and personal priorities. Most AI budgeting tools work from transaction data alone, which is rich but incomplete as a basis for comprehensive financial advice.

Robo-Advisors: Automated Investing That Has Proven Itself

Robo-advisors — automated investment platforms that build and manage portfolios based on user-provided risk tolerance, investment horizon, and goals — represent the most mature and most validated AI application in personal finance. The concept has been in production since Betterment launched in 2010, and the track record is now long enough to evaluate honestly.

The core value proposition is threefold: low cost (robo-advisors typically charge 0–0.25% annually versus 1–2% for human advisors), disciplined execution (automated rebalancing and tax-loss harvesting that removes the behavioural friction of manual portfolio management), and accessibility (minimum investment thresholds that have fallen to near zero for many platforms). Wealthfront claims their AI tax-loss harvesting adds 1–2% in annual after-tax returns — a material improvement that compounds significantly over a decade-plus investment horizon.

In India, SEBI-registered robo-advisory platforms including Scripbox, Groww’s automated portfolio tools, ET Money Genius, and Kuvera’s goal-based investment features provide domestically relevant versions of the robo-advisory value proposition — specifically adapted to Indian mutual fund structures, tax treatment (LTCG, STCG under current Finance Act provisions), and investment options rather than importing US-market portfolio models directly.

For simple situations, robo-advisors already handle portfolio management effectively. For complex situations — estate planning, tax strategy, business ownership — human advisors still add significant value. The emerging consensus is a hybrid model: AI for execution and routine optimisation, humans for strategy and complex decisions.

The honest limitation of robo-advisors is that their model quality — the underlying assumptions about return expectations, risk-return relationships, and optimal portfolio construction — varies significantly between platforms and is not always transparent. A robo-advisor built on sound academic evidence (factor-based portfolios, evidence-based rebalancing rules) is categorically different from one built on proprietary models whose basis is unclear. Evaluating the investment philosophy, not just the interface, matters for assessing which platform to trust with long-term capital.

AI Fraud Detection: The Invisible Protection That Works

AI fraud detection is the application where the technology’s impact is least visible to users and most consequential. Every time a suspicious transaction is flagged on your credit or debit card, every time your bank sends a security alert about an unusual login, every time an attempted payment is blocked because it does not match your typical behaviour — these are AI systems working in real time.

Over 70% of banks now use AI-driven fraud detection systems, making financial security better for everyday users. The technical approach is anomaly detection — machine learning models trained on vast datasets of transaction behaviour that identify patterns deviating from an established baseline. A transaction at an unusual location, an unusual time, for an unusual amount, at an unusual merchant category, following an unusual sequence of events, triggers model review. The model evaluates the combination of signals and decides whether to allow, flag, or block the transaction.

The improvement over rule-based fraud detection is substantial. Traditional fraud rules — block any transaction over ₹50,000 in a foreign currency — create both false positives (blocking legitimate transactions) and false negatives (missing fraud that does not match the rules). ML-based detection adapts to individual user behaviour and to evolving fraud patterns, producing significantly lower rates of both types of error.

Indian banks including SBI, HDFC Bank, and ICICI Bank, as well as the NPCI (National Payments Corporation of India) which operates the UPI infrastructure, use AI fraud detection systems that monitor billions of transactions for suspicious patterns. The NPCI’s real-time fraud monitoring across the UPI network is a structural advantage of India’s digital payments infrastructure — centralised monitoring at the network level catches patterns that any individual bank’s system would miss.

AI Credit Scoring: Expanded Access With New Risks

Traditional credit scoring — CIBIL, Experian, CRIF Highmark in India — assesses creditworthiness based on credit history: repayment track record, credit utilisation, account age, and credit enquiries. This model excludes a substantial population who have limited formal credit history despite having the income and discipline to service debt reliably — young earners, self-employed individuals, rural borrowers, and new-to-credit applicants.

Small-business funding has become very data-heavy and data-driven. Lenders are increasingly focusing on companies’ current cash flows and revenue streams when evaluating loan eligibility, aided by access to a trove of real-time financial data. AI credit scoring models extend this approach to individual borrowers — incorporating UPI transaction patterns, account cash flows, income consistency, spending behaviour, and in some implementations, alternative data sources like utility payment history and mobile phone usage patterns.

Fintech lenders including Slice, KreditBee, Freo, and MoneyTap have built credit products specifically targeting thin-file borrowers using AI-augmented credit assessment. The result has been genuine credit access expansion to borrower segments previously excluded from formal lending — but with important caveats.

The risk of alternative data credit scoring is that it can encode biases that are harder to identify and challenge than traditional credit criteria. If a model trained on historical lending data learns correlations between certain spending patterns or demographic indicators and loan performance, it may perpetuate historical inequalities rather than correcting them — particularly if the historical data reflects systematic discrimination in credit access. The Reserve Bank of India’s guidelines on responsible AI in financial services, issued in 2024, address model explainability and bias testing requirements for AI credit models, but implementation and enforcement remain works in progress.

The practical implication for borrowers: AI-powered credit products can be genuinely beneficial for thin-file borrowers who would be declined by traditional scoring. They should be approached with the same scrutiny as any lending product — interest rates, fees, repayment terms, and what data the lender is accessing and how it is used deserve careful evaluation.

AI Financial Planning: The Emerging Capability and Its Current Limits

The most consequential change AI brings to financial workflows in 2026 is not incremental efficiency but a fundamental shift in how systems understand intent, make decisions, and interact with humans. Financial workflows are moving from rigid, rule-driven processes to more adaptive, context-aware systems.

For individual users, this shift is most visible in AI financial planning assistants — tools that go beyond transaction categorisation to provide forward-looking analysis: projected cash flow, goal progress modelling, retirement projections, and scenario analysis. The value is making financial planning accessible to the population who cannot afford the ₹5,000–₹15,000 per hour that a qualified human financial planner charges and who previously had no access to personalised planning.

MIT Sloan professor Randall Kroszner raises the question of whether AI may become so personalised that it could advise people on what credit card to get or what savings account to open based on their circumstances, noting that this holds particular appeal for lower-income households, which are less likely to have access to a human financial adviser. This democratisation of financial guidance is the genuine long-term value proposition of AI in personal finance — quality financial thinking made accessible at scale.

The current limitation is that AI planning tools work from the data they have access to, which is often incomplete. A tool connected to your primary bank account sees your salary deposits and direct debit payments but not your fixed deposit at another bank, your PPF contributions, your EPF balance, your mutual fund holdings, or your real estate assets. Financial planning from an incomplete data picture produces incomplete recommendations — sometimes misleadingly so. Platforms that aggregate across multiple financial institutions (INDmoney’s multi-account aggregation, Perfios for professional users) address this limitation but require users to grant data access across all financial relationships, which raises the data privacy considerations addressed in the next section.

MIT Sloan professor Antoinette Schoar cautions that AI isn’t foolproof and that people still need to be able to ask the right questions and have enough financial sense to question what they’re being told. This is the critical literacy requirement for AI financial tools: the user needs enough financial understanding to evaluate whether the AI’s recommendation makes sense for their situation — not to be a financial expert, but to not outsource all judgment to an algorithm.

The Risks AI Introduces: What Most Users Are Not Told

Data Privacy: The True Cost of “Free” Financial AI

AI financial tools need access to your financial data to provide value. This is the core trade-off: the more comprehensively an AI tool understands your financial situation, the more useful its recommendations can be — and the more sensitive the data it holds about you.

Privacy concerns are prominent. J.P. Morgan Private Bank has described cases in which AI tools appeared to “know” sensitive details about a family after a family member used a free AI app, illustrating how conversational tools can aggregate data in ways users may not anticipate. Public AI tools can combine information from social media, online services, and user interactions in ways that may expose individuals or households to targeting.

The Indian regulatory context adds specific requirements. The Digital Personal Data Protection Act 2023 (DPDPA) establishes rights for data principals (users) including the right to access, correct, and erase personal data, and creates obligations for data fiduciaries (organisations processing data) including purpose limitation — using data only for the purpose for which consent was given. Financial apps that harvest transaction data for advertising targeting or sell data to third parties without clear disclosure are potentially violating DPDPA provisions. SEBI’s circular on digital lending and its guidelines for registered investment advisers also create specific data handling obligations for financial service providers.

Before connecting any AI financial tool to your bank accounts, evaluate: Is the platform regulated in India (SEBI-registered, RBI-licensed, or operating under an appropriate framework)? What data does it access and what does it use that data for beyond providing the service? Does it share or sell data to third parties? What are the data retention and deletion provisions? These questions have answers that should be available in the platform’s privacy policy — and a platform whose privacy policy does not clearly answer them warrants scepticism.

AI-Enabled Financial Fraud: The Threat That Scales Both Ways

AI enables more sophisticated attacks through deepfakes, synthetic identities, and convincing phishing in multiple languages. J.P. Morgan Private Bank advises verifying unexpected requests, especially those involving payments or sensitive information, through a separate channel. Criminals may create fake voice or video content of people known to the target, which is why “human authentication” steps such as a family safe word can be helpful.

In the Indian context, AI-powered fraud has taken specific forms that are increasingly common. Voice cloning scams that mimic family members requesting urgent UPI transfers. AI-generated phishing messages in Hindi, Tamil, Telugu, and other Indian languages that are grammatically perfect and contextually convincing in ways that earlier phishing attempts were not. Synthetic identity fraud using AI-generated documents that pass document verification systems not designed to detect AI-generated forgeries.

The most effective defence against AI-enabled fraud is not technical — it is procedural. An absolute rule that financial transfers requested through any communication channel are verified by calling back a known number (not a number provided in the communication) before execution eliminates the majority of UPI fraud, regardless of how convincing the request appears. The same verification principle applies to investment opportunities, loan offers, and any other financial action requested through incoming communication.

The most resilient approach is not blind trust in automation. It is intelligent use of AI within secure, transparent systems.

Algorithmic Bias and the Limits of Historical Data

AI systems learn from historical data. When historical data reflects systematic inequalities — in access to credit, in financial product availability, in income distribution — AI models trained on that data can perpetuate those inequalities even when no discriminatory intent exists in their design.

Research conducted at MIT Sloan on the credit card market found that less-educated and less financially sophisticated people were typically offered more confusing contracts and offer letters. AI systems that optimise for product engagement or approval rates without explicit fairness constraints can amplify this pattern — targeting more expensive or complex products at users whose financial literacy makes them less likely to evaluate the terms critically.

The regulatory response is developing. SEBI’s 2024 guidelines on AI in investment advisory require explainability for AI recommendations — advisors must be able to explain why the AI recommended a specific product. The RBI’s responsible AI framework for lending requires bias testing and fairness audits for AI credit models. These requirements are moving in the right direction; their enforcement consistency is still developing.

The AI Financial Tools Worth Knowing in India

For Budgeting and Spending Analysis

Fi Money — a digital banking product built specifically around AI-powered spending insights. The “Smart Deposit” and spending analysis features use transaction categorisation and pattern analysis to surface actionable insights from connected account data. Regulated as a banking partner of Federal Bank.

Jupiter — digital banking with AI spending analysis features, detailed transaction categorisation, and goal-based savings tools. Built on Federal Bank’s infrastructure and SEBI-registered for investment features.

INDmoney — multi-account financial aggregation that brings together bank accounts, mutual funds, stocks, US stocks, EPF, and fixed deposits into a single dashboard with AI-assisted insights across the full portfolio. The breadth of aggregation is the key differentiator for users who want a complete financial picture rather than single-account insights.

For Investing

Kuvera — goal-based mutual fund investment with direct fund access (no distributor commission), automated rebalancing, and AI-assisted portfolio recommendations based on stated goals and risk profile. SEBI-registered investment adviser.

Groww — the largest retail investment platform in India by user count, with AI-powered stock analysis tools and automated SIP management. The AI features are less sophisticated than dedicated robo-advisory platforms but are accessible within a platform most users are already familiar with.

Scripbox — one of India’s earliest robo-advisory platforms, focused specifically on goal-based mutual fund portfolios with evidence-based portfolio construction and automated rebalancing.

For Tax Planning

ClearTax — AI-assisted income tax filing and tax planning, with machine learning tools that identify applicable deductions from uploaded financial documents and suggest optimisation strategies. The AI document analysis capability that extracts data from Form 16, bank statements, and investment statements reduces the manual data entry that makes tax filing burdensome.

TaxBuddy — AI-powered tax advisory and filing with human CA oversight for complex situations. The hybrid model — AI for initial analysis and routine filing, human professional for complex or disputed situations — is the right structure for tax applications where errors have regulatory consequences.

How to Use AI Financial Tools Without the Risks

The practical framework for benefiting from AI in personal finance while managing its risks has four components.

Use regulated platforms exclusively for anything involving financial transactions or investment. SEBI-registered, RBI-licensed, or banking-partner-based platforms operate under regulatory oversight that creates accountability. Unregulated platforms that offer “AI financial advice” without regulatory authorisation are operating outside the framework that protects your interests.

Treat AI recommendations as inputs to your decision, not decisions themselves. An AI tool that recommends a specific mutual fund, suggests an insurance product, or advises increasing your SIP amount is providing a data-driven perspective — not fiduciary advice tailored to your complete situation. Evaluating whether the recommendation makes sense for your specific circumstances is your responsibility.

Apply strict verification to any financial action requested through incoming communication, regardless of how sophisticated or convincing the request appears. The verification rule — call back a known number before acting — defeats AI-powered fraud without requiring you to identify deepfakes or sophisticated phishing.

Read the data privacy terms before connecting financial accounts to any platform, and periodically revoke access for platforms you no longer actively use. Data access granted months ago to a platform you stopped using represents ongoing privacy exposure that account permission review can eliminate.

The Realistic 2026 Assessment

AI is not replacing financial planners, accountants, or investment advisers for complex financial situations. What it is doing — and doing with measurable impact — is automating the routine tasks that previously required either expensive professional time or discipline that most people cannot consistently sustain: spending categorisation, portfolio rebalancing, fraud monitoring, and tax-loss harvesting.

The difference in 2026 is not about whether a tool uses AI, but rather how that AI is designed, what it understands, and what it is trusted to do. An AI budgeting tool that works from a single bank account’s transaction data and an AI financial planning platform that aggregates your complete financial picture and applies sophisticated planning logic are both “AI” — they are not comparable in their capability or their value.

For most Indian personal finance users, the highest-value near-term AI applications are automated UPI transaction analysis to understand spending patterns, SIP automation and goal-based investing through SEBI-regulated platforms, AI fraud detection through banking apps and UPI monitoring, and AI-assisted tax filing through platforms like ClearTax. These applications are mature, regulated, and produce demonstrable value with manageable risk.

The more ambitious AI financial planning applications — comprehensive financial plan generation, AI-driven estate planning, fully personalised tax optimisation — are developing and will be significantly more capable in two to three years. Using the available tools now builds the data history and financial habits that make those more sophisticated capabilities more valuable when they arrive.

This article is written for informational and educational purposes only. It does not constitute personalised financial, investment, or tax advice. AI tools mentioned are cited for informational purposes and do not constitute endorsements. Always verify that any financial platform is appropriately regulated before connecting financial accounts or following investment recommendations. Consult a SEBI-registered investment adviser or qualified CA for personalised financial planning.