Personal Finance in India 2026: A Complete, Honest Guide to Managing, Saving, and Growing Your Money

Managing money in India in 2026 is simultaneously easier and harder than it has ever been.

Easier: UPI has made payments instant, zero-cost, and universal. Demat accounts open in minutes. Index fund SIPs run for ₹100 per month. Tax filing is partially automated. Digital insurance policies are issued in seconds. The infrastructure for responsible money management has never been more accessible.

Harder: The investment climate in 2026 is marked by heightened volatility. Equity markets may see a cautious start to the new year, with benchmark indices likely to move within a narrow range in the initial months, with factors such as uncertainty around India–US trade discussions, global geopolitical risks, overseas investor outflows, and a softer rupee acting as headwinds. Consumer debt is rising. Medical inflation continues at 12–14% annually. And the sheer volume of financial content — much of it designed to sell products rather than inform decisions — makes it harder than ever to know what to actually do.

This guide cuts through that noise. It covers every major dimension of personal finance for Indian individuals in 2026: budgeting, emergency funds, insurance, debt management, tax planning under the new framework, investing, and retirement — in the right sequence, with the right numbers, and with honest acknowledgment of what is uncertain.

Part 1: The Foundation — Getting the Sequence Right

The most expensive financial mistake most Indians make is not choosing the wrong investment. It is investing in the wrong order.

Financial experts are now urging a transition towards goal-based investing — a disciplined approach that aligns every rupee with a specific life milestone. Planning for 2026 requires more than just picking the right stocks. A comprehensive financial plan involves navigating new tax regimes, understanding market trends, and protecting your financial stability.

The right sequence — the order in which financial decisions produce the most value — is:

1 → Emergency fund (3–6 months of survival expenses in liquid instruments) 2 → Health insurance (adequate for family, not just employer cover) 3 → Term life insurance (if you have financial dependents) 4 → High-interest debt elimination (credit cards, personal loans above 15% APR) 5 → Tax-advantaged savings (80C instruments, NPS) 6 → Long-term equity investing (index fund SIPs) 7 → Goal-specific investing (home, education, retirement corpus)

Most people jump to step 6 while steps 1 through 4 are incomplete. The result is equity investments that get redeemed during medical emergencies at market lows, no insurance when it’s most needed, and debt that quietly erodes every rupee earned.

Work through this sequence before optimising at any individual step.

Part 2: Budgeting — The Skill That Makes Everything Else Possible

Budgeting does not mean tracking every rupee with spreadsheet obsession. It means knowing, with reasonable accuracy, where your money goes — so you can redirect it toward where it should go.

The 50-30-20 Framework Adapted for India

The popular 50-30-20 rule (50% needs, 30% wants, 20% savings) works as a starting point but needs adjustment for Indian realities — particularly for young professionals in metros where housing costs alone can consume 35–40% of take-home salary.

A more realistic framework for salaried Indians in 2026:

Non-negotiable fixed costs (target: 40–50% of take-home): Rent or EMI, groceries, utilities, transport, school fees, insurance premiums, loan repayments. These are committed — reducing them requires lifestyle change, not just willpower.

Variable discretionary spending (target: 20–30%): Dining, entertainment, clothing, travel, subscriptions. This is where most budget optimisation happens. Review quarterly.

Savings and investments (minimum: 20%, target: 30%+): This is the non-negotiable floor. Automate it to transfer on salary credit day — before you spend — using standing instructions in your net banking. The single most effective budgeting technique is paying yourself first through automation.

The survival number — the most important calculation you will do: Calculate your minimum monthly cost to keep your life operational: rent, basic food, utilities, transport to work, insurance premiums, EMI minimum payments. This is not your full budget — it is the absolute floor. This number tells you exactly how many months your emergency fund buys you in a genuine crisis.

Expense Tracking — Practical Tools for Indian Users

Manual spreadsheet tracking works for disciplined users. For most people, automation is more realistic:

Bank statement analysis (free): Most Indian banks now offer spending categorisation in their apps. HDFC SmartBuy, ICICI iMobile Pay, and Axis Mobile all provide monthly spend breakdowns. Use these before buying any third-party app.

UPI transaction history: PhonePe and Google Pay both provide monthly transaction summaries that reveal discretionary spending patterns most people are unaware of.

Dedicated apps: Walnut, Money View, and ETMONEY provide cross-account tracking with automatic categorisation. All are free at their useful tier. These apps access your SMS transaction notifications — verify the privacy policy before granting access.

Part 3: Emergency Fund — The Most Underrated Financial Tool

An emergency fund is not an investment. It is protection against being forced into terrible financial decisions during the worst moments of your life.

Without one: a medical emergency means breaking an FD at a penalty. A job loss means redeeming equity SIPs when markets are down — locking in losses permanently. A major repair bill means taking a personal loan at 18% interest.

Review your emergency fund: assess whether the existing reserve continues to cover around six months of current living expenses, factoring in any changes to income, spending patterns, or financial responsibilities.

How much: 3 months of survival expenses is the minimum. 6 months is appropriate if you are the sole earner, work in a volatile sector (startups, IT, media, gig work), or carry high fixed obligations (large EMIs, school fees).

Where to keep it — specific options with current May 2026 rates:

As of May 2026, leading commercial banks are offering FD interest rates ranging from around 6.1% to 7.1% for general depositors, with senior citizens typically earning an additional 50 basis points. For emergency funds specifically, shorter-tenure FDs or liquid funds are more appropriate than long-term FDs that penalise early withdrawal.

| Instrument | Current Yield (May 2026) | Liquidity | Best For |

|---|---|---|---|

| High-yield savings account (AU, IndusInd, YES Bank) | 6.0–7.0% | Immediate | Daily buffer (1 month) |

| Liquid mutual fund | 6.5–7.0% | T+1 business day | Primary emergency fund |

| Ultra-short FD (30–90 days) | 5.5–6.5% | At maturity | Predictable near-term needs |

| Standard savings account (SBI, HDFC) | 2.7–3.5% | Immediate | Too low — avoid for emergency fund |

The critical rule: Emergency fund money does not belong in equities, long-term FDs, or crypto — regardless of the potential returns. The moment you need emergency money is precisely when markets are most likely to be down and FD penalties most painful. Stability and liquidity take complete priority over returns in this bucket.

Part 4: Insurance — Protecting Before Growing

Insurance is the mechanism that prevents one adverse event from destroying years of financial progress. Two types are non-negotiable for anyone with financial responsibilities.

Health Insurance: The Urgency That Most Indians Underestimate

Medical costs in India continue to rise and can deplete savings rapidly. Medical inflation at 12–14% annually means a condition costing ₹2 lakh in 2020 may cost ₹3.5–4 lakh today. And employer group health insurance — which most salaried Indians rely on — stops the moment you leave the employer, precisely when financial stress is highest.

Minimum adequate structure:

Family floater: ₹15–₹20 lakh cover for a family of 3–4. In metro cities with private hospital costs at current levels, ₹10 lakh is the absolute floor and ₹20 lakh is more realistic for serious conditions. Annual premium for a couple aged 30–35 with one child from reputable insurers (Niva Bupa, Star Health, Care Health Insurance) ranges from ₹18,000–₹35,000 depending on cover amount and insurer.

Super top-up plan: Activates after your base policy’s sum insured is exhausted. A ₹40 lakh super top-up with a ₹10 lakh deductible (your base policy covers the deductible) costs dramatically less than equivalent base coverage. This combination — ₹10 lakh base + ₹40 lakh super top-up — gives ₹50 lakh of total coverage at the cost of roughly ₹10–15 lakh base coverage alone.

What to verify before buying any health policy:

- Claim Settlement Ratio from IRDAI’s latest annual report (above 90% is the baseline; below 85% is a red flag)

- Hospital network — verify your preferred hospitals AND the nearest government-empanelled hospitals are in-network

- Room rent sub-limits — policies capping room rent at ₹3,000/day in a city where standard rooms cost ₹8,000/day create significant out-of-pocket exposure

- Pre-existing disease waiting period (2–4 years; shorter is better)

- No-claim bonus structure — policies that increase sum insured for every claim-free year compound value over time

Term Life Insurance: Maximum Protection, Minimum Cost

A 30-year-old non-smoking male can get ₹1 crore of term life cover for 30 years for approximately ₹8,000–₹12,000 per year from HDFC Life, ICICI Prudential, or Max Life. This is 2–3 restaurant meals per month for ₹1 crore of family protection.

The calculation: Cover needed = amount that, invested conservatively at 7% return, generates your current annual income. Annual income ₹6 lakh ÷ 0.07 = ₹85.7 lakh. Round up to ₹1 crore.

The product to avoid: ULIPs (Unit Linked Insurance Plans) and traditional endowment plans bundle insurance and investment but deliver poor results in both dimensions. Insurance coverage is typically inadequate relative to need; investment returns trail simple index fund SIPs significantly. The commissions on these products are among the highest in the Indian financial industry — which explains why they are aggressively sold at bank branches and by insurance agents.

The principle: buy term for protection. Invest separately through mutual funds. Keep insurance and investment completely separate.

Part 5: Tax Planning Under the Income Tax Act 2025

Tax planning in 2026 requires an understanding of the statutory framework governing income taxation in India. The Income Tax Act 2025 now forms the basis of tax computation for Tax Year 2026–27. Enacted through the Finance Act 2025, it replaces the earlier statute and reorganises several provisions. The fundamental choice for taxpayers remains: assessing whether tax efficiency will arise from lower slab rates and rebate mechanisms under the New Tax Regime, or from investment-linked deductions available under the Old Tax Regime.

New Tax Regime vs. Old Tax Regime — The Decision Framework

From April 1, your tax-saving limits reset under various sections like 80C. This allows investors to plan investments in instruments such as ELSS, PPF, and NPS in a structured manner. The new financial year 2026–27 is a fresh start to take control of your finances with clarity and discipline.

New Tax Regime (default):

- Zero tax for net taxable income up to ₹12 lakh through Section 87A rebate

- Lower slab rates above ₹12 lakh

- No deductions under 80C, 80D, HRA, home loan interest, or standard deduction

- Best for: individuals earning under ₹12 lakh net, those with minimal deductions, those who prefer simplicity

Old Tax Regime (opt-in required at ITR filing):

- Deductions available: ₹1.5 lakh under Section 123 (equivalent to old 80C), ₹25,000–₹50,000 under 80D, HRA exemption, standard deduction

- Higher slab rates before deductions; lower effective rate after claiming all eligible deductions

- Best for: individuals earning above ₹15–₹20 lakh with significant legitimate deductions (home loan interest, large 80C investments, full health insurance premium, HRA in metro cities)

How to decide: Add up every deduction you can legitimately claim in the old regime. Subtract from your gross income. Calculate the tax under both regimes using ClearTax’s free comparison tool or the Income Tax Department’s calculator at incometax.gov.in. Choose whichever produces lower total tax outgo.

Section 123 (formerly 80C) — ₹1.5 Lakh Deduction

Section 123 of the Income Tax Act 2025, which corresponds to the earlier Section 80C structure, provides deductions for specified investment-linked instruments under the Old Tax Regime.

The key instruments and their specific characteristics in 2026:

ELSS (Equity Linked Savings Scheme): The only 80C instrument investing in equities. 3-year lock-in — shortest among all 80C options. Historically the highest-returning 80C instrument because equity growth over the long term exceeds fixed-income alternatives. In the old regime, LTCG above ₹1.25 lakh per year is taxed at 12.5% (post Budget 2024). For investors with 5+ year horizons, ELSS is typically the optimal 80C choice.

PPF (Public Provident Fund): NSC rate is around 7.7% per annum for January–March 2026. PPF offers government-backed fixed returns with EEE (Exempt-Exempt-Exempt) tax status — contributions deductible, growth tax-free, withdrawals tax-free. Current PPF interest rate for Q1 FY 2026-27 is 7.1% per annum. 15-year lock-in (extendable in 5-year blocks). Guaranteed by Government of India. The gold standard for risk-averse savers and the safe-harbour component of any 80C portfolio.

NSC (National Savings Certificate): The National Savings Certificate remains a reliable and secure government-backed investment instrument for individuals who want fixed returns with tax benefits and capital safety in 2026. The rate is around 7.7% per annum, unchanged for the January–March 2026 quarter. Interest is compounded annually but paid only on maturity. Yes, under Section 80C up to ₹1.5 lakh. NSC has a fixed 5-year lock-in period. It is backed by the Government of India and considered risk-free.

Tax-Saving FD: Tax saving FDs vs regular FDs: fixed deposits continue to remain a preferred investment option for conservative investors seeking stable and predictable returns. In May 2026, leading commercial banks are offering FD interest rates ranging from around 6.1% to 7.1% for general depositors. 5-year lock-in. Interest is fully taxable at your slab rate — this is a critical difference from PPF and NSC. For investors in the 30% bracket, the effective post-tax return is approximately 4.3–4.9% — below current inflation in many scenarios.

EPF (Employee Provident Fund): For salaried employees, EPF contributions automatically qualify under Section 123. The employer’s 12% of basic salary contribution + your own 12% = 24% of basic salary invested in EPF monthly, often filling a large portion of the ₹1.5 lakh limit without additional action.

NPS — The Additional ₹50,000 Deduction

The National Pension System provides an exclusive additional deduction of ₹50,000 under Section 80CCD(1B) — over and above the ₹1.5 lakh Section 123 limit. For a taxpayer in the 30% bracket, this saves ₹15,000 in tax immediately — a guaranteed 30% return on that contribution before any market return is considered.

NPS, EPF, and private pension schemes are key retirement accounts for Indian investors. The sooner you start, the more compounding works in your favour, making early planning critical.

At retirement, 60% of the NPS corpus can be withdrawn tax-free; 40% must be used to purchase an annuity (which is taxable as income). The locked-in nature of NPS Tier 1 — with partial withdrawal allowed only after 3 years for specified purposes — is a feature for retirement savings, preventing impulsive redemption during market downturns.

Section 80D — Health Insurance Premium Deduction

Health insurance premiums qualify for deduction under Section 80D (old regime):

- Self, spouse, dependent children: up to ₹25,000 per year (₹50,000 if any member is a senior citizen)

- Parents additionally: up to ₹25,000 (₹50,000 if parents are senior citizens)

A family adequately insured with ₹25,000 in annual premiums saves ₹7,500 in tax at the 30% bracket. The insurance is simultaneously sensible protection and a tax deduction — buy it for the protection, benefit from the deduction.

Part 6: Debt Management — The Highest-Return Investment

Paying off a credit card balance at 36% APR is mathematically equivalent to earning a guaranteed, tax-free 36% return. No equity fund, no real estate investment comes close. For anyone carrying high-interest debt, aggressive repayment is the most impactful financial decision available.

Young India has got into a mountain of debt. Indians still do not have student debt to the extent other countries have, but there are other forms of debt that are rising. In the last few years, banks and NBFCs have focused on consumer lending and Indians have lapped up loans at fairly high rates of interest.

The True Cost of Indian Credit Card Debt

Credit card interest in India ranges from 28% to 42% per annum — among the highest in any major economy. The minimum payment trap is particularly destructive. Paying only the minimum on a ₹50,000 balance at 36% APR means the balance takes over 4 years to clear even with consistent minimum payments, and you pay more in interest than the original purchase amount.

The debt avalanche (mathematically optimal): List all debts by interest rate. Pay minimum on all. Direct every additional rupee toward the highest-interest debt first. Once cleared, roll that payment into the next-highest. This minimises total interest paid across all debts.

The debt snowball (psychologically effective): Pay off the smallest balance first for a quick motivational win. Slightly more interest paid overall, but the momentum generated often sustains the effort longer. Use this if the avalanche feels overwhelming and you aren’t starting.

The rule before investing: Do not start new investments (beyond Section 123 minimum and emergency fund) while carrying credit card debt or personal loans above 15% APR. The guaranteed return of debt elimination exceeds any realistic investment return at that interest rate.

Part 7: Investing for Long-Term Growth

The Market Context for Indian Investors in May 2026

Based on the growth trajectory seen over the past decade, where industry assets have expanded at an annualised pace of around 20 percent, the sector is widely expected to reach a significant milestone in 2026, with total assets under management approaching the one trillion dollar mark. At the same time, passive investment strategies are gaining traction at a faster rate than traditional actively managed funds, reflecting a growing preference for cost efficiency and index-linked returns.

Fixed deposits continue to be viewed as a relatively stable savings avenue. Current trends suggest that bank interest rates may have limited scope for further increases, while sharp cuts also appear unlikely in the near term. In the bond market, attention remains on the government’s borrowing plans for FY27.

This context suggests: equity markets offer long-term growth potential but near-term caution is warranted. Fixed income remains relevant for conservative allocations. The strategy for individual investors is not to predict direction but to invest consistently through cycles.

SIP — Why Consistency Beats Market Timing

A Systematic Investment Plan invests a fixed amount in a mutual fund at fixed intervals. The mechanism that makes it powerful is rupee cost averaging: when markets fall, your fixed SIP amount buys more units. When markets rise, accumulated units are worth more. Over a long horizon, this averages out volatility and produces returns close to the fund’s actual long-term performance — something that market timing almost never achieves.

The compounding mathematics are significant. A SIP of ₹5,000 per month started at age 25, assuming 12% CAGR (approximate long-term historical average for large-cap Indian equity), grows to approximately ₹1.77 crore by age 55. Started at 35, the same SIP reaches approximately ₹50 lakh — less than a third, for ten fewer years.

Small habits like tracking expenses weekly, avoiding lifestyle inflation, and starting early with investments compound into powerful results in the long run.

Index Funds vs. Active Funds — The Evidence

Passive investment strategies are gaining traction at a faster rate than traditional actively managed funds, reflecting a growing preference for cost efficiency and index-linked returns.

SPIVA India reports (Standard and Poor’s independent index performance tracking) consistently show that the majority of actively managed large-cap funds underperform the Nifty 50 index over 5–10 year periods after fees. The reason is structural: the expense ratio advantage of index funds (0.05–0.20% vs. 1.0–1.8% for active funds) compounds into a significant drag that most active fund managers cannot consistently overcome.

Practical index fund choices for Indian investors (May 2026):

| Fund | Index | Expense Ratio (Direct) | Best For |

|---|---|---|---|

| Nippon India Nifty 50 Index Fund | Nifty 50 | ~0.10% | Core large-cap exposure |

| UTI Nifty 50 Index Fund | Nifty 50 | ~0.18% | Reliable, well-established |

| UTI Nifty Next 50 Index Fund | Nifty Next 50 | ~0.28% | Mid-large cap diversification |

| Motilal Oswal Nifty 500 Index Fund | Nifty 500 | ~0.25% | Broad market, one fund solution |

| Mirae Asset Nifty Midcap 150 Index Fund | Nifty Midcap 150 | ~0.28% | Mid-cap allocation |

Always invest in Direct plans. Regular plans pay a distribution commission to your bank, mutual fund distributor, or app — reducing your return by 0.5–1.0% annually. Over 20 years, this difference on a ₹5,000/month SIP is several lakhs of foregone wealth. Direct plans are available through the AMC’s own website, Zerodha Coin, Groww Direct, Paytm Money’s direct option, or MFCentral.

Asset Allocation — The Framework That Protects You

A smart strategy involves diversifying your portfolio to balance risk and reward. Rebalance once a year to keep your plan aligned.

Asset allocation based on time horizon:

Money needed within 3 years: 0% equity, 100% debt instruments (liquid funds, short-duration FDs, debt funds). Market downturns can take 2–3 years to recover — money needed within this window cannot absorb that volatility.

Goals 3–7 years away: 30–40% equity (index funds via SIP), 60–70% debt (medium-duration debt funds, PPF contributions, NSC). Partial equity adds growth potential; debt anchors against volatility.

Goals 7+ years away: 70–80% equity (Nifty 50 + Nifty Next 50/Nifty 500), 20–30% debt (PPF, NPS, short-duration debt funds). Long horizons absorb equity volatility and benefit most from compounding.

Annual rebalancing: Once per year, check actual allocation vs. target. If equities have grown to 85% of a portfolio targeted at 70%, sell some equity and buy debt to restore the target. This systematically enforces “sell high, buy low” without requiring market judgment.

Gold — How Much and in What Form

Gold serves as a portfolio stabiliser — holding value when equities fall and when the rupee weakens. A 5–10% allocation is reasonable for Indian households both for cultural relevance and portfolio function.

Most cost-efficient forms in 2026:

Sovereign Gold Bonds (SGBs): Government-backed bonds denominated in grams of gold. Provide 2.5% annual interest (taxable) plus gold price appreciation. Capital gains on maturity after the 8-year term are completely tax-free. The most tax-efficient form for long-term gold exposure. Monitor the RBI calendar for upcoming SGB tranches.

Gold ETFs: Trade on NSE and BSE like shares. Expense ratios 0.15–0.50%. More liquid than SGBs (can sell any time at market price). LTCG after 24 months taxed at 12.5% without indexation (post Budget 2024 changes). Lower transaction costs than physical gold.

Physical gold (coins/bars from authorised dealers): Acceptable for cultural and ornamental purposes. For pure investment, SGBs and Gold ETFs are superior due to zero storage risk and better cost efficiency.

Avoid: Digital gold sold through payment apps (PhonePe, GPay, Paytm). These are not SEBI-regulated securities, carry private-operator custody risk, and have higher costs than SGBs or Gold ETFs.

Part 8: Retirement Planning — The Goal Most Indians Under-Prepare For

India’s average life expectancy has crossed 70+ years. A person retiring at 60 may need to fund 25–30 years of living expenses. With inflation at 5–6% annually, ₹60,000/month of current expenses requires approximately ₹2,10,000/month in 25 years to maintain the same purchasing power.

Planning for this is not pessimistic — it is the responsible default.

The Retirement Corpus Calculation

A practical formula:

- Estimate monthly expenses in retirement (today’s rupees)

- Subtract expenses that will end (EMIs, school fees, work transport)

- Add new retirement expenses (higher healthcare, leisure, home maintenance)

- Multiply annual requirement by 25 (the inverse of the 4% sustainable withdrawal rate)

Example: Monthly retirement expenses ₹70,000 → Annual ₹8,40,000 → Corpus needed = ₹8,40,000 × 25 = ₹2.1 crore (in today’s rupees). Adjust this for inflation to find the nominal corpus needed at your retirement date.

NPS as the Retirement Wrapper

NPS offers multiple tax benefits, making it an attractive option for retirement planning. Contributions to NPS qualify for deduction under Section 80C, and an exclusive additional deduction of ₹50,000 is available under Section 80CCD(1B) for contributions to NPS. If your employer also contributes to your NPS account, that contribution is deductible under Section 80CCD(2).

The forced illiquidity of NPS Tier 1 — lock-in until retirement with partial withdrawals only for specified purposes — is a feature for long-horizon investors. It prevents the reactive redemption during market downturns that destroys long-term returns for equity investors who lack discipline.

EPF — The Automatic Retirement Savings Most Indians Underuse

For salaried employees, EPF is the primary retirement savings vehicle by default. The 12% + 12% employer-employee contribution structure builds a substantial corpus over a 30-year career. The current EPF interest rate is 8.25% for FY 2025-26 — higher than most fixed-income alternatives and fully tax-free on corpus withdrawal after 5 continuous years of contribution.

What most EPF holders don’t know: Withdrawing EPF when changing jobs — a common practice — permanently destroys the compounding effect of those contributions. Transfer your EPF account (using the EPFO’s online transfer facility through your UAN) when changing employers rather than withdrawing. The transferred corpus continues compounding. A withdrawal triggers TDS (if less than 5 years of service) and permanently removes that capital from your retirement corpus.

Part 9: The New Trends Shaping Indian Personal Finance in 2026

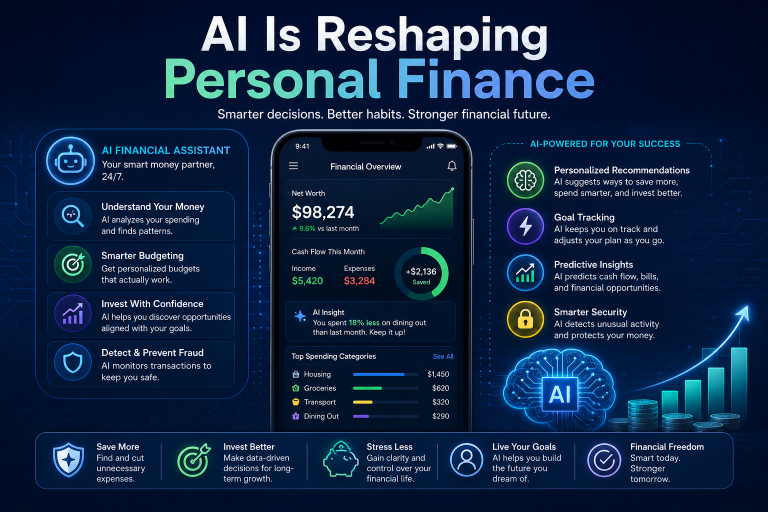

AI-Assisted Financial Planning

Artificial intelligence is making machines more intelligent and helping them use judgment to make decisions with large data. The investment world is going to get more complex. Financial planners will have to be adequately equipped to make smart use of technology and individuals must look at ways and means of using AI more fruitfully. Imagine an AI engine that can predict future movement in rates, equity indices, and tax rates and position your asset mix accordingly.

AI-powered tools are now embedded in mutual fund platforms, tax filing software, and portfolio management apps. ClearTax uses AI for optimised tax regime selection. Groww uses AI for portfolio analysis. The value: faster computation and broader data synthesis than any individual can manually achieve.

The caution: AI financial tools are only as good as the assumptions built into them. They optimise for stated parameters — which may not fully capture your actual life circumstances, risk tolerance, or goals. Use them as decision support, not as a replacement for understanding your own finances.

ESG Investing Gaining Ground

ESG investment is well-known in India although it is yet to pick up in a big way as a strategy. In the coming year, we are likely to increasingly see people insisting that their investments match up with their value systems. Investments in cigarette, liquor, and gambling companies could be taboo for some investors. The focus will increasingly be on aligning long-term wealth with value systems.

SEBI has mandated enhanced ESG disclosure by listed companies, and several AMCs now offer ESG-screened index funds. For investors for whom ethical alignment matters alongside returns, this category is expanding meaningfully in India.

The Wealth Transfer Opportunity

The biggest shift will be the great wealth transfer that will happen in India and the world over the next few years. UBS projected that nearly $83 trillion of wealth will be transferred to the next generation in the next 20 years. Millennials and Gen-Z are likely to see a massive growth in their wealth starting 2026, much of which will be inherited. Financial planners will need to closely work with individuals on managing a tax-efficient transition of wealth.

For families expecting to receive or pass on significant assets: consult a CA and estate planning specialist well before the transfer. Gift tax implications, capital gains on inherited assets, and the structuring of family arrangements all have tax consequences that poorly planned transfers create unnecessarily.

Digital Banking Regulation Tightening

As digital banking becomes the norm, the RBI and other regulators are tightening rules on fraud. In 2026, banks must obtain explicit customer opt-in for digital services. Critical banking systems must be isolated from peripheral apps by a 2028 deadline. Two-factor checks now include more biometrics and analytics layered over traditional OTPs. The Digital Personal Data Protection Act is now in full force, with penalties for breaches reaching up to ₹250 crore.

For individual users: expect stricter KYC requirements, more frequent re-authentication on banking apps, and enhanced scrutiny on large digital transactions. These are protective measures — not inconveniences.

Part 10: Common Financial Planning Mistakes — What to Avoid

Mistake 1 — Buying insurance-investment combos: ULIPs and endowment plans have commissions that reduce your return and insurance coverage that is inadequate relative to need. Separate insurance (term) from investment (mutual funds) entirely.

Mistake 2 — Over-relying on FDs: Efficient tax planning can save significant money, while debt management ensures financial stability. FD interest is fully taxable at your slab rate. At 30% bracket, a 7% FD returns approximately 4.9% post-tax. Against 5–6% inflation, real returns are marginal to negative. FDs belong in emergency funds and short-term goal buckets, not as a complete investment strategy.

Mistake 3 — Redeeming SIPs in downturns: This converts a temporary paper loss into a permanent real loss. Market downturns are when SIPs buy the most units for the same rupee — redemption during downturns is the exact opposite of rational long-term investing.

Mistake 4 — Ignoring EPF transfer when changing jobs: Withdrawing EPF on job change sacrifices compounding, triggers TDS, and permanently reduces retirement corpus. Always transfer — use EPFO’s online portal with your UAN.

Mistake 5 — Chasing recent top performers: The mutual fund with the highest 1-year return in any category almost always reverts toward category average within 2–3 years. Selecting funds based on recent performance is one of the most consistently documented investing errors in retail investor behaviour studies.

Mistake 6 — No annual review: Review the asset mix to assess whether any holdings have grown disproportionately compared to others. Periodic rebalancing helps maintain alignment with the original asset allocation and risk profile, especially after phases of uneven market performance.

Your Starting Checklist — Five Actions This Week

If the scope of this guide feels overwhelming, start with these five actions:

- Calculate your survival number (minimum monthly cost to function). Write it down. This anchors every other financial decision.

- Open a liquid fund account (Zerodha Coin, Groww, or directly through any AMC’s website). Transfer whatever you can spare — even ₹2,000. This starts your emergency fund.

- Check your health insurance cover. If you rely solely on employer insurance below ₹5 lakh, get quotes for a ₹10 lakh family floater at PolicyBazaar or Ditto Insurance this week.

- Start one Nifty 50 Direct Plan SIP — ₹500 per month minimum. Set the date 2 days after your salary credit. Automate it and don’t check it for 3 months.

- Calculate which tax regime suits you for FY 2026-27 using ClearTax’s free comparison tool. Submit your preference to your employer’s payroll by the date they require (typically April–May of the financial year).

None of these five actions requires more than two hours. All of them will materially change your financial trajectory compared to continued delay.

This article is for educational and informational purposes only. It does not constitute personalised financial, investment, insurance, or tax advice. All investment decisions carry risk, including possible loss of principal. Interest rates and tax provisions are accurate as of May 2026 and subject to change. The Income Tax Act 2025 provisions described reflect the framework as of publication date — consult the income tax department website (incometax.gov.in) or a Chartered Accountant for the most current provisions. Past performance of any investment is not indicative of future returns. Consult a SEBI-registered investment adviser for personalised investment guidance.

Author: Mahesh — independent personal finance writer covering Indian financial markets since 2019. No affiliate relationships with any financial product, fund, bank, insurance company, or platform mentioned in this article. No compensation received from any entity referenced.